Introduction

As we move into Q2 2025, the mortgage market remains highly competitive, with major lenders vying for business and specialist lenders adapting to shifting borrower needs. While there is positive momentum - particularly in the first-time buyer (FTB) segment - economic uncertainty, regulatory changes, and affordability pressures continue to shape trends in the mortgage market.

In this quarter’s Specialist Lending Trending, Adrian Moloney, Group Intermediary Director at OSB Group, examines the key developments driving the market and the opportunities ahead for brokers and lenders alike.

Market Trends

Interest rates and mortgage affordability

The start of 2025 has been marked by intense competition among lenders, especially in the high-street banking sector, with many adjusting pricing strategies to capture market share. This has led to greater affordability in some areas, but challenges persist due to economic factors such as budget changes (notably in national insurance) and fluctuating interest rates.

Despite affordability concerns, purchase activity has increased, particularly among first-time buyers looking to secure deals before impending stamp duty changes take effect. We’re also seeing a rise in higher LTV products.

Homebuyer demand & borrower segments

The market had a hectic start to 2025, with strong buyer demand carrying over from Q4 2024. Brokers are seeking stability amid uncertainty, particularly ahead of any changes in Chancellor Rachel Reeves's spring budget announcement.

Due to the stamp duty shift, FTBs remain the most active segment, but the impact on the wider market remains to be seen. Traditionally, the spring season sees a pick-up in transactions, though broader economic conditions - including interest rates and regulatory adjustments - will dictate the pace.

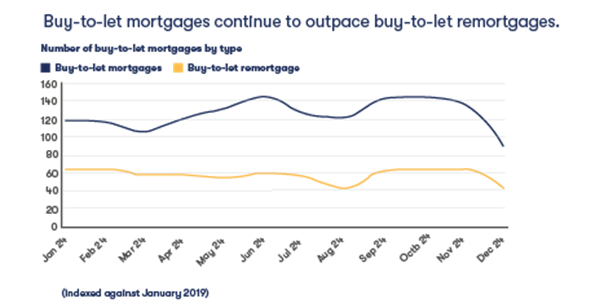

Buy-to-let (BTL) remains stable, with a new generation of landlords emerging. While professional landlords are focused on profitability and EPC compliance, younger and new-market landlords - particularly millennials - are entering the market with a more aspirational mindset.

Diversified opportunities

One of the big shifts we’re seeing so far this year is the rise of bridging and commercial finance as core broker opportunities. Traditionally overlooked, these sectors are now becoming essential tools in a broker’s arsenal.

Bridging finance, once considered a niche product, is proving to be a vital solution for chain breaks and short-term funding gaps. With lenders refining their criteria and increasing flexibility, more brokers are recognising the value of offering bridging as part of their service suite.

Commercial lending is another major growth area. Many self-employed clients already have commercial borrowing needs - whether it’s buying a premise, expanding operations, or refinancing existing assets - but they often aren’t aware their mortgage broker can help. Brokers who proactively introduce these options can unlock new revenue streams while strengthening client relationships.

The broker opportunity

For brokers, the next three to six months present a significant opportunity. Educating clients about bridging and commercial finance, as well as diversifying offerings, will be critical. Many brokers already have clients with specialist needs, but the key lies in asking the right questions and leveraging existing relationships.

Technology will continue streamlining processes, but ultimately, service quality and lender consistency remain the top priorities for brokers and their clients. The most successful brokers will be those who position themselves as trusted advisors, offering not just the cheapest rate but the right solution.

Our Pick of the Charts

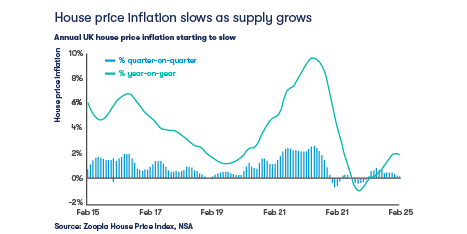

Zoopla House Price Index: March 2025

House price inflation slows as supply grows

House price inflation is starting to slow after a sustained recovery over the last 12 months. The annual rate of UK house price inflation edged lower in February to 1.8%, down from 1.9% in January.

Zoopla House Price Index: March 2025

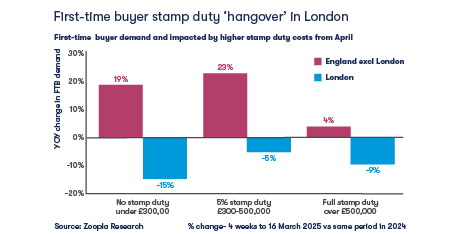

First-time buyer stamp duty ‘hangover’ in London

Many first-time buyers (FTB) bought forward decisions to buy homes late last year to avoid paying higher stamp duty from 1 April 2025.

Connells Group Q4 2024 Market Report

Number of buy-to-let mortgages by type